はじめに

米現地日付2021年6月15日(火)にAT&T(T)の最高財務責任者(CFO)Pascal Desroches氏がCredit Suisse 23rd Annual Communications Conferenceで株主への最新情報アップデートに関して講演を行った。

AT&T経営陣の株主へのアップデート(Updates Shareholders)は5月24日のJ.P. Morgan Global Technology, Media and Communications Conferenceにおける最高経営責任者John Stankey CEO以来となるが、その際はその前に発表されたワーナーメディアのスピンオフ関連の補足説明が主体だった。

今回の発表はそのアップデートからしばらく経過しており、ワーナーメディアのスピンオフばかりに目が行きがちであったAT&T全体の見通しについて確認する良い機会と思われるので、以下にその内容を整理しておく。

Credit Suisse 23rd Annual Communications Conferenceでの最高財務責任者(CFO)Pascal Desroches氏の講演まとめ

以下はAT&Tの企業サイトより引用・抜粋。

【モビリティ】

- in the most recent quarters, AT&T’s mobility strategy of focusing on the long-term value of its high-value customer base has been successful in reversing previous subscriber losses.

直近の四半期では、価値の高い顧客ベースの長期的な価値に焦点を当てるAT&Tのモビリティ戦略は、以前の加入者の流出を逆転させることに成功しています - These gains, coupled with the ongoing opportunities to drive out costs through the transformation of the company’s distribution channels, gives AT&T confidence in its ability to continue to deliver profitable postpaid subscriber growth.

これら加入者の獲得は、会社の流通チャネルの変革を通じてコストを削減する継続的な機会と相まって、AT&Tが収益性の高い後払い加入者の増加を提供し続ける能力に自信を与えています

【ネットワーク】

- AT&T’s network is performing as well as it ever has and that as the company accelerates its deployment of C-band spectrum, it expects to cover 200 million people by the end of 2023, strengthening its ability to deliver even faster average speeds across the country and to densify its network as demand for 5G grows and the use cases for the technology expand.

AT&Tのネットワークはこれまでと同じように機能しており、同社がCバンドスペクトルの展開を加速するにつれ、2023年末までに2億人をカバーすると見込んでいおり、全国でさらに高速な平均速度を提供する能力を強化すると見込んでおり、5Gの需要が高まり、テクノロジーのユースケースが拡大するにつれて、全国でさらに高速な平均速度を提供し、ネットワークを高密度化する能力を強化します - the company’s outlook includes expectations for continued elevated wireless competition and thus recent promotional activity by other wireless providers does not come as a material surprise

同社の見通しには継続的なワイヤレス競争の激化への期待が含まれており、他のワイヤレスプロバイダーによる最近のプロモーション活動は重大な驚きではありません

【ファイバー】

- the company’s plan to double the size of AT&Ts fiber footprint to about 30 million customer locations by year-end 2025 should open up new use cases and opportunities given the company’s integrated fiber deployment strategy and penetration trends in areas where fiber has already been deployed.

2025年末までにAT&Tのファイバー展開規模を2倍の約3000万の顧客ロケーションに拡大するという同社の計画は、同社の統合ファイバー展開戦略とファイバーが既に展開されている地域での普及傾向を考えると、新しいユースケースと機会をもたらすはずです

【ワーナーメディア】

- expects WarnerMedia’s second-quarter results to benefit from positive comparisons to the second quarter of 2020, which represented the worst of the pandemic impacts in that business unit.

ワーナーメディアの第2四半期結果は、ビジネスユニットにおけるパンデミックの影響の中で最悪の結果であった2020年の第2四半期とのポジティブな比較の恩恵を受けると予想しています - in the second half of the year, he expects WarnerMedia to benefit from improvements in advertising revenues, a return to theaters and run rate benefits from the second-half 2020 restructuring.

今年の下半期は、ワーナーメディアが広告収入の改善、劇場への復帰、2020年下半期のリストラによるランレートの恩恵を受けると予想しています - expressed confidence in the upcoming planned international launch of HBO Max and in the company’s ability to deliver on its guidance of 67 to 70 million HBO Max customers by the end of 2021.

HBO Maxの今後計画されている国際的な展開と、2021年末までに6700万から7000万人のHBO Max加入者というガイダンスを提供する同社の能力に自信を示しました

【スピンオフ】

- 以前に提供したスピンオフ完了後2022~2024年のガイダンスは変わらず

- Low-single digit revenue CAGR and mid-single digit adjusted EBITDA and adjusted EPS CAGR.

1桁台前半の収益CAGR(年成長率)と1桁台半ばの調整済みEBITDAおよび調整済みEPS CAGR - The company expects to generate $20 billion plus in free cash flow on an annual basis post-close, with a dividend payout ratio in the 40% to 43% range for a total dividend payout of $8 billion to $9 billion per year.

決算後の年間ベースで200億ドル以上のフリーキャッシュフローを生み出し、配当支払い率は40%から43%の範囲で、年間配当総額は80億ドルから90億ドルになると見込んでいます - the company expects to increase capital investment to around $24 billion annually, focused on 5G and fiber.

同社は5Gとファイバーに焦点を合わせて、設備投資を年間約240億ドルに増やすと見込んでいます - The company also expects net debt to adjusted EBITDA in the 2.6x range after the transaction closes, moving to less than 2.5x by year-end 2023.

同社はまた、取引終了後純負債が調整後EBITDAの2.6倍の範囲となり、2023年末までに2.5倍未満になると予想しています - AT&T expects to have the optionality to repurchase shares once net debt to adjusted EBITDA is less than 2.5x.

AT&Tは、調整後EBITDAの純負債が2.5未満になると、株式を買い戻すオプションがあると予想しています

- Low-single digit revenue CAGR and mid-single digit adjusted EBITDA and adjusted EPS CAGR.

- the company doesn’t expect to reset the current dividend until after the proposed WarnerMedia-Discovery transaction is approved and closed.

提案されたWarnerMedia-Discoveryトランザクションが承認されて終了するまで、現在の配当をリセットする予定はありません

まとめ

以上内容を整理してみたが特に目新しい情報は無し。まとめるほどの事も無かったかと思わないでもないが、逆に考えると7月22日に予定されている第2四半期決算発表のひと月前の時点で特筆すべき悪材料が無いとも言える(単に開示していないだけかもしれないが)。

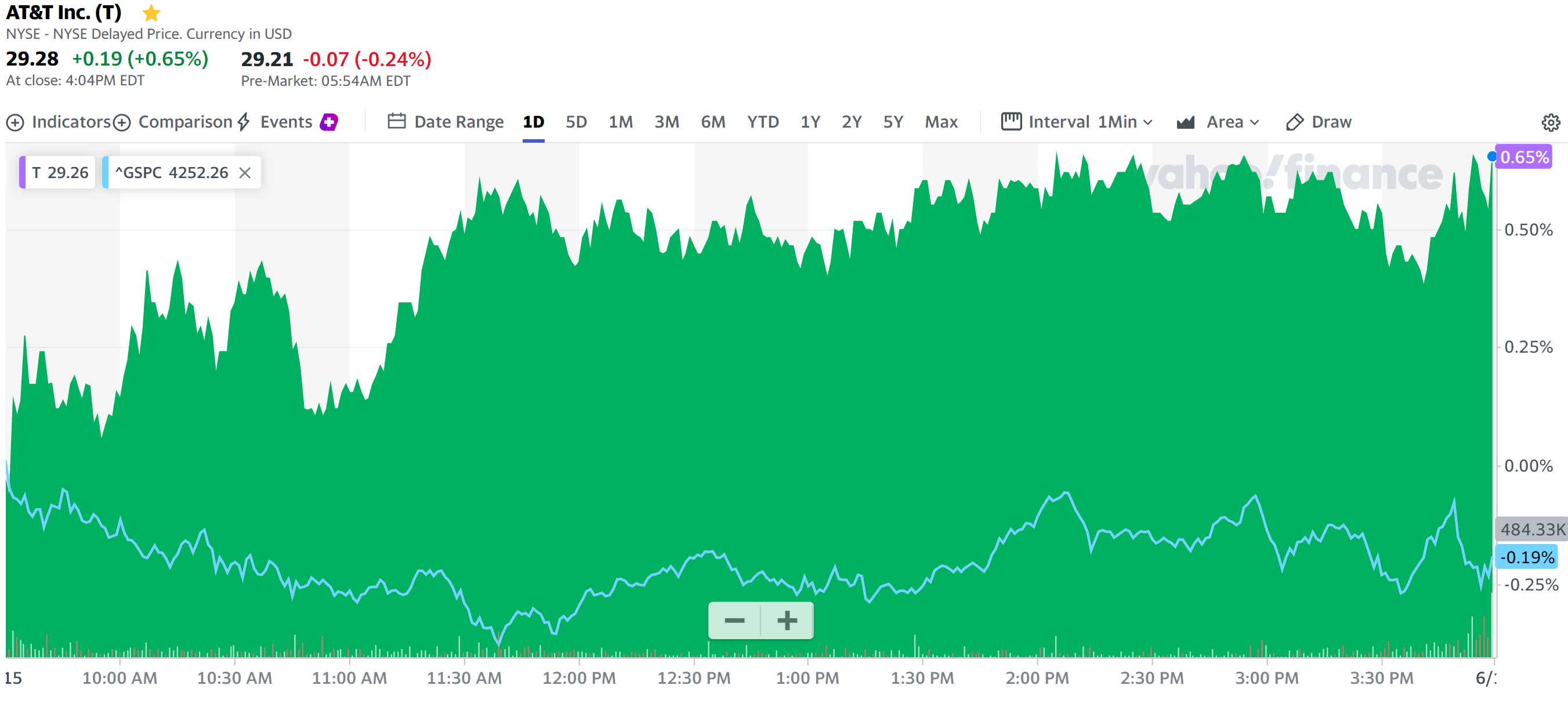

この講演が行われたのは米東部時間10時15分なのだが同日のAT&Tの株価の動きは

11時前後に下落しているが、講演開始以降午前中S&P 500が下げ基調であったのに対して上昇基調であったことから、市場にそれなりに評価されたのではないかと思う。

7月22日に予定されている第2四半期決算まで特にイベントなどの講演は予定されていないので、株価が落ち着いた動きをしてくれればと思うのだがどうなるか。