はじめに

昨日2023年5月22日(月)の(恐らく市場取引後)に掲題のAT&T(T)最高経営責任者(CEO)John Stankey氏がJ.P. Morgan Technology, Media and Telecommunications Conferenceで講演を行い最新情報のアップデートを行った。

以下、アップデートの内容及びAT&T株の動きを確認しておく。

J.P. Morgan Technology, Media and Telecommunications ConferenceにおけるAT&T最高経営責任者John Stankey氏のアップデート

以下はAT&Tの企業ページより引用・抜粋。

【財務関連】

- Stankey reiterated his confidence in the company’s ability to deliver free cash flow of $16 billion or better for full-year 2023.

Stankey氏は、同社が2023年通年で160億ドル以上のフリーキャッシュフローを実現できるとの自信を改めて表明した - His confidence reflects expectations for continued adjusted EBITDA growth of 3%+ for the year, driven by steady operational execution and ongoing benefits from the company’s cost reduction initiatives.

同氏の自信は、着実な業務遂行と会社のコスト削減イニシアチブによる継続的な利益によって、年間の調整後EBITDAが3%以上の成長を続けるという期待を反映している - Stankey expects that handset payments peaked in the first quarter and will be lower for full-year 2023 compared to 2022.

Stankey氏は携帯端末の支払い額が第1四半期にピークに達し、2023年通年では2022年と比較して減少すると予想している - Additionally, he expects capital investment to be broadly in line with guidance for the remainder of 2023, following a year-over-year increase in the first quarter.

さらに設備投資は第1四半期の前年比増加に続き、2023年の残り期間も概ねガイダンスと一致すると予想している

【ワイヤレス関連】

- Stankey said he expects second-quarter postpaid net additions to be influenced by three factors:

Stankey氏は第2四半期の後払い純増は以下の3つの要因に影響されると予想している- A continued normalization of industry growth;

業界成長の継続的な正常化 - Temporary impacts from competitor rate plan launches; and

競合他社の料金プラン開始による一時的な影響、及び - The one-time reduction of about 75,000 customers from a government contract AT&T opted not to pursue given its uneconomic return profile.

AT&Tが不経済な収益プロファイルを考慮して追求しないことを選択した政府契約による約75000ユーザーの1回限りの削減

- A continued normalization of industry growth;

- Absent these impacts, the company has not seen a material shift in share across the wireless industry, including to new cable MVNO offerings.

こうした影響がなければ、同社は新しいケーブルMVNO(Mobile Virtual Network Operator:仮想移動体通信事業者)サービスを含めワイヤレス業界全体でシェアに大きな変化は見ていない

【ネットワーク関連】

- The company remains on track with its network expansion commitments and expects to deploy midband spectrum to 200 million people by year-end 2023 and to pass 30 million+ customer and business locations in its traditional service area with fiber by the end of 2025.

同社はネットワーク拡大への取り組みを順調に進めており、2023年末までに2億人にミッドバンドスペクトルを展開し、2025 年末までに従来のサービスエリアで3000万以上の顧客と事業所をファイバーでつなぐと予想している - Stankey believes AT&T’s position as the largest-scale domestic fiber builder gives it an advantage in managing costs despite build and labor costs that have moderately impacted the company’s fiber build.

Stankey氏は、AT&Tが国内最大規模の光ファイバー企業としての地位を確立しているため、同社の光ファイバーにある程度の影響を与えている製造コストと人件費にもかかわらずコスト管理において有利であると考えている - In addition, AT&T is already seeing lower maintenance and repair costs where fiber has been deployed. The combination of better initial penetration rates and higher ARPU levels have improved the return case on AT&T’s fiber investments.

さらに、すでにファイバーが導入されている場所ではメンテナンスと修理のコストが削減されており、初期普及率の向上とARPUレベルの向上により、AT&Tの光ファイバー投資の収益率は改善している

まとめ

実際のカンファレンスでは先日の2023年第1四半期決算でフリーキャッシュフローが大きく市場予想を下回ったことを市場がどう見るかの認識についてJohn Stankey氏は「I was wrong(私は間違っていた)」と述べた上で、上記に挙げたAT&Tのサイトにまとめとして掲載された市場を安心させる内容に繋げている。

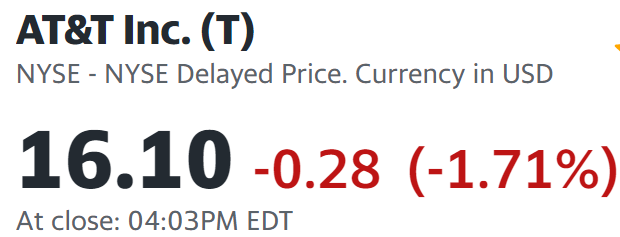

しかしカンファレンスを受けての23日(火)のAT&T株(Stankey氏の講演は22日(月)の取引時間後)は

前日比1.71%の減少。同日の米国市場が

いずれも冴えない結果だったのに比べても割と大きな下げ幅となっており、講演内容は市場に評価されなかったようだ。

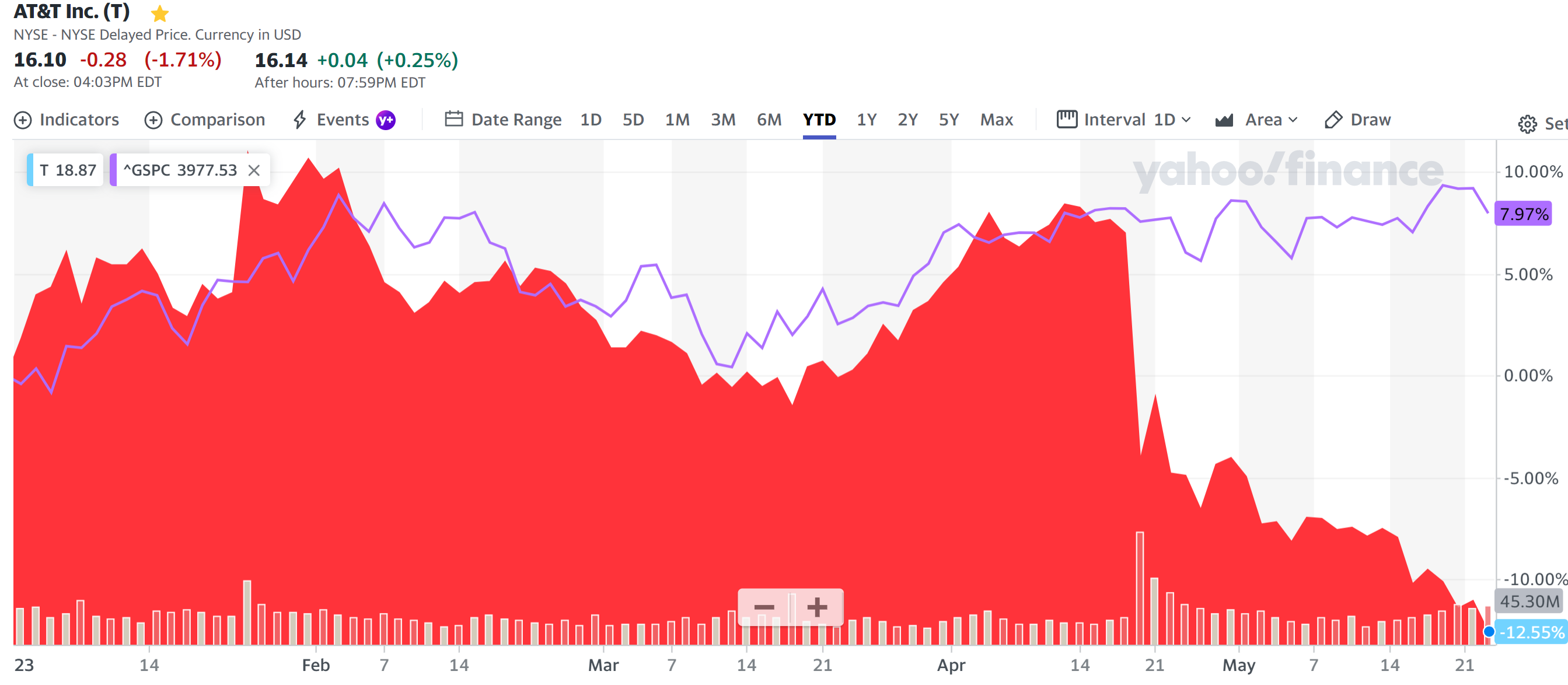

年初来のAT&T株は

先日の2023年第1四半期決算で大幅に下落して以降下落基調が続き、年初来ではS&P 500が約8%上昇しているのに対し約12.5%のマイナスとなっている。

前回の四半期決算時には

「気になる今後だが、フリーキャッシュフローに関する懸念を払拭する情報が提供されない限り株価が大きく上昇することは見込めないだろう。」

と書いていたのだが、四半期決算時の下落ではその懸念を吸収しきれずその後も株価下落が続いてしまっている。

今後のAT&T株だが、こういった講演でのアップデートなどで具体的にキャッシュフローの改善が言及されない限りは弱気な株価推移が続きそうな気がする。いつかはキャッシュフローの懸念が株価に反映されて、この下げ基調が止まってくれることを期待したいのだが正直しばらくはAT&T株にとって厳しい日々が続くことを覚悟しておいた方がいいだろう。